Towards an Analytical Discipline of Forkonomy

Note: This work was written and self-published in manuscript form

on pllel.com in summer 2018 with last

revision 10th

August.

Figures come from tweets, original manuscript and presentation slides

from ETC Summit Forkonomy

talk in September

2018. A follow-up commentary was

published

in early 2019.

Abstract

This work introduces a novel field of cryptocurrency research that the

author terms forkonomy, and provides a general overview of recent

phenomena in this area. Attention is directed towards the first UTXO

consolidation fork-merge combining Zclassic and Bitcoin ledger

histories into the so-called Bitcoin Private network. Potential

implications for ageing blockchain ecosystems, prominent minority

cryptocurrency network fragments and divergent factions are discussed.

1. Introduction and Literature Review: The Hitherto Canon of Forkonomy

1.1 Forkonomy, Forks and Forkability

With respect to cryptocurrencies, forkonomy can be considered to

constitute the study of the fragmentation of software codebases and

protocol networks comprising distributed communities and/or stakeholders

operating in a permissionless or trust-minimised manner. Much as

astronomy utilises observation and theory to understand and predict

cosmological characteristics and phenomena, here follows an analogous

attempt to apply blockchain analytics and historical precedent to with a

view to understanding fundamental and emergent characteristics of the

forking tendencies of divergent monetary network factions.

In the open source computer science domain, the notion of project

codebase forks is well established and occurs when an existing piece of

software develops in diverging paths by independent developer

constituencies, creating separate and distinct pieces of software.

Torvalds' original Linux kernel from 1991 has been forked into countless

descendant projects [1]. With the launch of the Bitcoin network in

2009, the prospect of provable digital scarcity and secure decentralised

open source value transfer protocols was realised. This was implemented

through the novel combination of systems networking, UTXO (Unspent

Transaction Output) based accounting, resilient data architecture,

cryptography and thermodynamic elements [2]. With a permissionless

ledger system employing a blockchain and triple-entry accounting to

reach a high degree of probabilistic transaction finality over time,

there exists the prospect of both codebase and ledger forks [3].

For the purposes of this work, a blockchain is defined as a temporally

sequenced, linear and append-only data structure employing cryptography

to facilitate the implementation of a high assurance, tamper-evident

transaction ledger.

A codebase fork of a cryptocurrency corresponds closely to the

relationship between Linux kernel forks, creating an independent project

typically launched with a new genesis block which may share consensus

rules but with an entirely different transaction history than its

progenitor. An example of this relationship type is that between Bitcoin

(BTC) and Litecoin (LTC) and this method may be thought of as a static

fork insofar as there is little time-sensitivity to the process. By

contrast, a ledger fork creates a separate incompatible network, sharing

its history with the progenitor network until the divergent event,

commonly referred to as a chain split.

Consensus rule changes or alteration of the network transaction history

may be the cause of such a fracture, deliberate or unplanned. This

occurrence may be regarded as a dynamic fork since the process takes

place in real time. Often when networks upgrade software, consensus

rules or implement new features a portion of the network participants

may be left behind on a vestigial timeline that lacks developer,

community, wallet or exchange support. Recently a fifth of nodes running

Bitcoin Cash (BCH) --- a SHA-256 minority ledger fork of BTC with

significantly relaxed block size limitations --- were separated from the

BCH network and a non-trivial number of would-be nodes remain

disconnected from the canonical BCH blockchain at time of writing weeks

later [4].

1.2 What Maketh a Fork?

The distinction between what constitutes a vestigial network and a

viable breakaway faction is unclear and difficult to objectively

parameterise. There is a significant element of adversarial strategy,

political gamesmanship and public signalling of (real or synthetic)

intent and support via social media platforms. The notions of critical

mass and stakeholder buy-in are ostensibly at play since ecosystem

fragmentations would be characterised as strongly negative sum through

the invocation of Metcalfe's Law as regards network effects and hence

value proposition [5]. Any blockchain secured thermodynamically by

Proof-of-Work (PoW) is susceptible to attack vectors such as

so-called 51 % or majority attacks, leading to re-orgs (chain

re-organisations) as multiple candidates satisfying chain selection

rules emerge. These can result in the potential

for double-spending the same funds more than once against entities

such as exchanges who do not require sufficient confirmations for

transaction finality to be reliable in an adversarial context. Should a

network fragment into multiple disconnected populations, adversaries

with control of much less significant computational resource would be in

reach of majority hashrate either using permanent or rented computation

from sources such as Nicehash or Amazon EC3 [6].

A striking example of this was the divergence of the Ethereum developer

and leadership cadre (ETH) from the canonical account-oriented Ethereum

blockchain (ETC) due to the exploitation of a flawed smart contract

project resembling a quasi-securitised decentralised investment fund

known as The DAO (Decentralised Autonomous Organisation) [7]. In

this case the Ethereum insiders decided to sacrifice immutability and by

extension censorship-resistance in order to conduct an effective bailout

of DAO participants which came to exercise Too-Big-To-Fail influence

over the overall Ethereum network, insider asset holdings, token supply

and mindshare [8]. A social media consultation process in conjunction

with on-chain voting was employed to arrive at this conclusion though

both methods are known to be flawed and gameable [9]. During

the irregular state transition process akin to a rollback, a

co-ordinated effort between miners, exchanges and developers took place

on private channels, exposing the degree of centralisation inherent in

the power structures of constituent network participants.

The key event which transformed the canonical Ethereum blockchain (where

the DAO attacker kept their spoils) from a vestigial wiped out chain

to a viable if contentious minority fork was the decision by Bitsquare

and Poloniex exchanges to list the attacker's timeline as Ethereum

Classic (ETC) alongside high-profile mining participants such as

Chandler Guo, well resourced financial organisations such as Grayscale

Invest (a subsidiary of Digital Currency Group) and former development

team members such as Charles Hoskinson to publically declare and deploy

support, developers and significant hashrate to defend the original

Ethereum network [10]. ETC now exists as an independent and sovereign

network with diverging priorities, characteristics and goals to ETH as

discussed in Section 4.

1.3 Transient Fork Dynamics in PoW Networks

At a granular level, blockchains grow in height incrementally as new

valid blocks are found by miners or validators and added to the

canonical chain as determined by the network's chain selection rules. In

PoW consensus mechanisms this leaderless race is conducted through the

combination of nonces (an arbitrary variable cycled through

sequentially) with the proposed block header to generate hashes which

are then compared against the network difficulty which is closely

related to the quantity of computational resource directed at the

network. Should a hash be found that is below the network's difficulty

requirements, given that no other consensus rules have been violated in

the process of constructing the candidate block then it is typically

considered valid by the network. As the miner announces the proposed

block it propagates across the network typically via a gossip protocol,

whereby nodes broadcast all messages to connected peers.

Since cryptographic hash functions are deterministic (albeit with with

unpredictable outputs) and a broad subset of possible hash values

satisfying the difficulty requirements exist, it is entirely plausible

that more than one valid candidate block may be found by competing

miners at very similar times. In such an eventuality there begins a

block propagation competition of sorts which serves to allow the network

to reach consensus on the latest state of the transaction ledger. Since

there can only be one block with a particular height, should multiple

candidates emerge the prospect of network partition arises if subsets of

the population of validating nodes do not overwhelmingly agree on the

latest block.

Such partitions may be short-lived in the case of orphans and uncles

which represent discarded timelines as the canonical chain built upon

another candidate block. The term uncle is used primarily in

Ethereum-based networks, as a partial subsidy is allocated to orphaned

blocks and therefore acts as a consolation prize for producing a valid

block which does not become part of the canonical chain. Ethereum

currently subsidises uncles with approximately 3000 ETH per day which

equates to over 1 million USD at time of writing [11]. Increasing

orphan rates may also be indicative of malicious behaviour on a network

such as 51 % attacks, selfish mining or distributed denial of service

vectors on reachable nodes which accept incoming peer connections.

Due to the message propagation characteristics of partially synchronous

distributed systems such as peer-to-peer (P2P) cryptocurrency networks,

there exists an inverse relationship between the median inter-block time

(more commonly referred to as the block time) as set by the protocol ---

600 seconds in BTC/BCH and 15 seconds in ETH/ETC --- and the incidence

of orphans and uncles. With shorter block times the likelihood of orphan

blocks increases, with some mitigating effect possible through miners

aggregating together co-operatively into so-called mining pools. A

similar effect of increasing orphan rate would also be expected should

the utilisation of block capacity also increase, as larger amounts of

information must propagate around the network nodes. ETH uncle rates

have been increasing since October 2017 due to mining subsidy reduction,

network congestion and increasing block size, whilst ETC's has remained

more consistent, due at least in part to the lower transactional volume

on the canonical Ethereum chain [12].

There may be a fundamental basis rooted in natural science that provides

insight into the increasing forking tendencies of blockchains. These

phenomena may be a result of entropic bias, that is to say divergent

paths are those of least resistance in accordance with Newtonian

physics. The second law of thermodynamics states that the total entropy

(energy unavailable to do useful work) of a closed system undergoing an

irreversible process can never decrease. In other words, all that can be

done is to arrest the descent of order into chaos is to continue

applying effort so as not to allow the amount of available energy to

decrease. In the context of network forks, a simple model may be

constructed of a PoW cryptocurrency network as a closed thermodynamic

system with a growing blockchain (an irreversible process) with mining

participants' cryptographic hashing as the work going into the system.

Taking this a step further, despite the ongoing work in the system a

chain split would satisfy the second law of thermodynamics as it

pertains to increasing disorder in a system. Therefore it may be the

case that the energetic dynamics of cryptocurrency networks provides a

rational basis for the eventuality of ledger forks in networks which do

not strongly penalise or prevent them.

Another issue widely encountered with ledger forks are replay attacks.

In the case where two recently partitioned network fragments share

identical or very similar codebases and transaction histories, unless

specific measures are taken there exists the very real prospect that a

network user wanting to send cryptocurrency may inadvertently send the

transaction on both network fragments and therefore have the transaction

accidentally replayed. Replay protection may be achieved through a small

codebase change which allows networks to distinguish transactions as

arising from one particular fragment. A related issue which may see an

increase in incidence as a result of the development of protocols

facilitating the issuance of non-native assets, tokens and off-chain

payment channels atop blockchains is the lack of precedence in the event

of a fork and chain split in the base layer. As off-chain protocols

proliferate and grow in intricacy, functionality and interoperability

this issue is likely to increase in complexity.

Selfish mining --- also known as block withholding - is a postulated

attack vector most effectively employed by mining oligopolists on a PoW

network with relatively long block times. It may be conducted by a miner

who finds a valid block but instead of immediately broadcasting to

peers, the block is withheld and kept secret. The miner then begins to

search for a valid block atop the previous clandestine block, with the

aim of finding a valid second block before another participant finds an

alternative valid first block. It has been claimed that this strategy is

more beneficial than honest mining for a sufficiently well-resourced

adversary, with 2013 research finding that Bitcoin is vulnerable to

block withholding attacks when an adversarial entity controls as little

as a quarter of the total computational resource possessed by the

network. [13] Naturally this is a far lower bound than the majority

hashrate required for 51 % attacks. However the efficacy of this attack

vector has been disputed more recently with findings that the strategy

only performs well in the period immediately after a difficulty

adjustment. With that in mind, a fairly minor change to the Bitcoin

protocol (albeit requiring upgrade consensus) could be effected to

mitigate the possibility of this attack [14].

Selfish mining is potentially relevant to forks as chain splits may be

more likely in the presence of selfish mining participants. A possible

heuristic for selfish mining is the issuance of empty blocks (to capture

efficiency in propagation time) that Bitmain-controlled mining pool

Antpool regularly mined for long periods of time despite network

congestion and foregoing transaction fees, indicating a potential

benefit greater than an honest miner's payoff of block reward and

transaction fees [15]. There is evidence that a selfish mining attack

possibly took place in May 2018 on Monacoin, a Japanese cryptocurrency

network, with a succession of blocks only containing the coinbase

(mining subsidy) transaction between block heights 1329837 and 1329846.

However it is not straightforward to differentiate between 51 % and

selfish mining attack vectors as the culprit definitively. As Monacoin's

difficulty adjustment occurring every block the window of opportunity

for selfish mining is somewhat limited and the attacker's spoils

corresponded to less than 100000 USD at time of the attack [16].

Stubborn mining builds on this methodology to facilitate a wider range

of hybrid strategies between honest and selfish mining extremes [17].

Zhang et al. proposed a selfish mining disincentivisation and

fork-resolving policy improvement for BTC chain selection ruleset having

explored censorship-attack vectors such as blacklisting via

feather-forking [18] as originally characterised hypothetically by

Miller in 2013 [19].

Feather-forking can be understood as a strategy available to mining

participants (more likely pools than individual entities) to refuse to

construct blocks atop a timeline which contains unfavourable

transactions within the recent history. By doing so the feather-forking

participant may also incentivise other mining participants to also join

the feather-fork for a short time. However this vector is rendered

ineffective provided that a majority of the computational resource

remains honest. Zhang and coauthors propose a mitigating upgrade to

Bitcoin named Publish or Perish which would slightly modify the chain

selection rule to include all hashes of orphaned blocks in the block

currently being worked upon. However the stringent synchronicity

assumptions in the proposed initial framework do no match the

characteristics of typical cryptocurrency networks and no provision is

made against chain splits or intentional forks [20].

1.4 Forks and Network Governance

For a range of reasons, there is often strident resistance to hard forks

--- irreversible protocol upgrades or relaxing of the existing consensus

ruleset --- in trust-minimised cryptocurrency networks such as BTC. The

lack of controlling entities may lead to a chain split and network

partition if the delicate balance of orthogonal stakeholder incentives

fails in the presence of a potential divergent event. The implementation

of Segregated Witness (SegWit) by the BTC network was eventually

achieved in 2017 as a backward-compatible soft fork following several

years of intense political and strategic maneuvering by the constituent

stakeholders in the BTC network. This off-chain governance process of

emergent consensus requiring de facto supermajority or unanimity

measured by miner signalling has proven to be an inefficient and

gameable mechanism for administering the BTC network [21]. Certain

stakeholder constituencies such as the developers maintaining the

reference Bitcoin Core software client implementation of BTC could not

easily reach agreement with mining oligopolists and so-called big block

advocates over the optimum technological trajectory for the BTC network.

The solution combined a fix for transaction malleability and network

capacity increase through the restructuring of block contents,

principally through the addition of a second Merkle tree which includes

witness (signature) data but excludes coinbase transactions. This was

initially conceived as a hard fork, and was only found to be

implementable as an opt-in soft fork due to inventive engineering.

Despite this, major stakeholders of the mining constituency strongly

opposed SegWit as it would render a previously clandestine proprietary

efficiency advantage known as covert ASICBoost ineffective on the

canonical BTC chain [22]. A grassroots BTC community movement

campaigning for a so-called User Activated Soft Fork (UASF) for SegWit

implementation and a face-saving Bitcoin Improvement Proposal (BIP91)

from mining farm operator James Hilliard in tandem facilitated the

eventual lock-in of the SegWit upgrade in the summer of 2017 [23].

A new and contentious network partition took place in August 2017 as

SegWit locked in for later activation, giving rise to the Bitcoin Cash

(BCH) network which rejected SegWit and instead opted for linear

on-chain scaling. This was implemented in the form of block size

increases which have the effect of externalising network resource burden

onto node operators, chiefly in the form of increased bandwidth and

storage performance requirements. BCH continues to be regarded as a

hostile ledger fork of BTC owing to its constituency of high-profile

personalities claiming that their network more closely resembles the

initial whitepaper specification of the Bitcoin protocol [24] and

therefore qualifies as the "real Bitcoin". By contrast, PoW --- also

known as Nakamoto consensus - selects the canonical BTC blockchain as

the chain with the most accumulated difficulty that satisfies the

consensus rules as laid out in the original Satoshi client codebase and

Bitcoin whitepaper. By changing the block size and loosening the

consensus ruleset without overwhelming agreement from all constituencies

of the BTC network, it is difficult to find a basis for BCH proponents'

claims to be the canonical Bitcoin blockchain without invoking appeals

to emotion, authority or other logical fallacies. The continuing

presence of Craig S. Wright and his claims to be a progenitor of Bitcoin

are an example of these attempts at legitimacy [25], though these

claims do appear to be substantially weakening.

1.5 Forks and Networks Employing Proof-of-Stake

Alternatives to Nakamoto consensus such as Proof-of-Stake (PoS) and

various approaches to Byzantine Fault Tolerance (BFT) are the subject of

active exploration in distributed systems research and development. In

foregoing the utilisation of brute thermodynamic force to secure the

network, PoS consensus protocols must satisfy through alternative means

the properties of persistence and liveness. Persistence pertains to the

immutability of the transaction history and liveness relates to network

synchrony, in that valid transactions will be included in the ledger

reliably.

Algorand promises fork-resistance through a novel block minting process

employing an accelerated BFT mechanism with constantly changing

committees being tasked with block proposal privileges. This protocol

has yet to be implemented in a permissionless setting and concerns

persist over intellectual property protection and the architecture of

stakeholder incentives within the network [26] as there is currently

no provision for validator subsidy upon block creation. In pure

Proof-of-Stake systems such as Ouroboros there is no thermodynamic

element to assign block creation privileges and instead rights are

conferred based on control of coin balances.

This results in a different set of fork-based challenges to PoW-oriented

networks discussed above. The nothing-at-stake problem arises from the

lack of significant resource cost in maintaining multiple timelines in a

pure PoS network. In PoW networks resource must be committed to find

valid blocks and therefore a significant penalty exists for malicious

actors to maintain multiple blockchain timelines. In PoS this penalty is

small or absent and therefore it is feasible to proliferate multiple

timelines branching from various points in the chain with little

drawback if one such fork fails and is not built upon substantially.

Nothing-at-stake also raises the possibility of re-orgs should an

adversary acquire enough "old stake" from wallets that no longer control

balances in the current ledger but previously did. Once sufficient old

stake is amassed, the user can then begin to build upon alternative

timelines in order to outrun the honest timeline and therefore become

the canonical chain should the selection rules not provide protection

against this approach. The long-range attack employs nothing-at-stake to

seed Byzantine network nodes with dishonest timelines such that a node

joining the network can face significant challenges in determining which

is the canonical blockchain.

Stake grinding is an attack vector class observed in early PoS

implementations employed by Blackcoin, Peercoin and NXT, where block

validators take measures to game the "randomness" of validator selection

and/or block creation privileges in their favour by grinding - or

sequentially searching through parameter space --- for a dishonest edge

over the intended working of the block creation mechanism [27]. The

Cardano network's proposed PoS-based consensus mechanism family

Ouroboros claims to have addressed these attack vectors by employing

sophisticated cryptographic elements such as Verifiable Random Functions

and Genesis Proofs to facilitate stake-based finality, provable security

and dynamic availability such that nodes may join the network at any

time and bootstrap from genesis. However implementation into the public

Cardano network has yet to take place, so the security model of

Ouroboros is yet to be tested in the wild [28].

Given the significant downside potential of real and perceived threats

to the resilience and legitimacy of a fragmenting network and loss of

associated network effects, the ability of a blockchain-based protocol

network to demonstrate fork resistance provides significant strength to

its value proposition. Decred is an example of a hybrid PoW/PoS monetary

network which is implementing an off-chain proposal and governance

mechanism termed Politeia [29]. Since coin-holders have voting rights

based on stake weight, they have the ability to keep miners and

developer constituencies honest through the mechanism to reach decisions

by majority stakeholder consensus on matters including hard forks. These

lessons were ostensibly learned through the developer team's experiences

in writing a BTC client which they felt was not appraised objectively by

the Bitcoin Core developer ecosystem. Decred's fork resistance is

effectively achieved by the fact that most stakeholders would be

non-voting on a minority chain, it would remain stalled as blocks would

not be created or propagated across the upstart network.

Recently another class of fork has emerged, caused by factionalisation

before networks launch and/or code is open sourced. These appear similar

to contentious political factions in existing blockchain networks though

there is little concrete information in the public sphere. Recently

several distinct entities have arisen within the pre-functional Tezos

ecosystem who do not support the decisions of Dynamic Leger Solutions

(DLS) as they move towards launching their mainnet, particularly

regarding the recent decision to require de-anonymising

Know-Your-Customer (KYC) information from their 2017 token offering

donations taken last year which raised the equivalent of several hundred

million USD. Aside from the ostensible paradox of rather security-like

donations requiring Anti-Money Laundering (AML) procedures for future

claims on the DLS-Tezos network, at the time of writing three

alternative proposed non-KYC implementations exist: TzLibre, nTezos and

OpenTezos. Little is publically known about these groups, but the

effective bifurcation of the pre-functional network into white KYC and

black non-KYC populations is a phenomenon likely to repeat as blockchain

forensic tools become more widely adopted by law enforcement agencies

[30]. At time of writing, Tezos has an operational betanet and TZLibre

appears to have adjusted strategy, becoming a leading delegated staker -

or baker in the Tezos parlance - within the DLS-Tezos network and

campaigning for a reversal of the KYC implementation decision.

1.6 Forks in Favour of ASIC-Resistance

Since SHA-256 Application Specific Integrated Circuits (ASICs) were

first developed in 2012 for the Bitcoin network, there has been a trend

among upstart networks to choose alternative hashing algorithms so as to

avoid the problems associated with being a minority network in relation

to a particular type of computational resource. A series of existing and

new algorithms such as Scrypt, CryptoNight, Blake 2b, Ethash and

Equihash with greatly increased memory requirements relative to SHA-256

were implemented into networks such as Litecoin, Monero, Siacoin,

Ethereum and Zcash respectively, under the supposition that

memory-hardness would prevent the development of ASICs for these

algorithms as the ability to parallelise processes would be greatly

reduced via the system memory bottleneck. Such algorithms were commonly

referred to as ASIC-resistant, however this does not appear to have

remained the case as there now exist ASICs for all of the above hash

functions.

The failure to prevent specialised hardware development was unavoidable

in retrospect. As cryptocurrency network valuations increased the

incentives for equipment manufacturers to allocate the substantial

capital to develop specialised integrated circuits outweighed the

downside risks. Other contributing factors were optimisations in mining

hardware engineering, steps forward in semiconductor manufacture and

margin compression in the more mature SHA-256 ASIC marketplace

encouraging hardware manufacturers to diversify. As the mining hardware

business is extremely competitive, development of ASICs for new

algorithms was conducted with utmost secrecy so participants would not

lose their early-mover advantage. Indeed it is commonly accepted (if not

conclusively proven) that many mining manufacturers will mine in secret

prior to announcing their equipment and offering units for sale. Light

testing of electronic equipment prior to despatch is uncontroversial as

part of a quality assurance process, however there have been widespread

accusations that ASIC manufacturers --- or partners for the purposes of

plausible deniability --- deploy ASICs to networks clandestinely and

gradually with hashrate spread over several pools to avoid detection

[31]. Further, there have been a number of instances whereby a new

ASIC type would be announced (by a manufacturer such as Baikal,

Innosilicon or Bitmain) and an impression of limited run scarcity would

be implied, to maintain a value proposition for the profitability of the

device. There would then follow what may be regarded as supply dumping

where the manufacturer sells so many ASICs that the possibility of a

purchaser achieving a return on investment would be nil. There is also a

question mark over the network security of cryptocurrencies with

clandestine ASICs online, as an equipment manufacturer "testing" large

batches of their equipment would have an asymmetric edge over existing

participants employing Central Processing Unit (CPU), Graphics

Processing Unit, (GPU) or Field-Programmable Gate Array (FPGA) and may

easily garner a majority of network hashrate making 51 % attacks

trivial, with grave impact on network value proposition. Some networks

that have adopted the philosophy of ASIC-resistance --- with the goal of

maximising decentralisation at the mining level --- reacted to the

suspicion or discovery of ASICs on their network by proposing a fork

(hard or soft depending on the circumstances) to change the hashing

algorithm to an alternative candidate sufficiently distinct from the

original so as to render the ASICs ineffective. As in all cases with

forks to irreversibly change mining parameters on PoW networks, should

sufficient computational resource remain on the original chain then it

has a prospect of avoiding wipeout and surviving as a sovereign network.

In this case where large quantities of ASICs were produced and then

threatened with being rendered incompatible through hashing algorithm

adjustment, these machines would most likely be obliged to remain on the

original chain, or to switch to mining on a smaller network which did

not undergo such a fork. It has been postulated that new CPU

architectures such as Vector Processors may be present in current or

forthcoming generations of ASICs which would allow for a greater ability

to remain on their intended network after hard forks to change hashing

algorithms. By analysing the limited efficiency gains in ASICs developed

for memory-hard algorithms such as Ethash compared to those observed

previously realised for SHA-256, an alternative technical configuration

with greater computational flexibility than traditional ASICs is a

plausible though unconfirmed hypothesis [32].

Providing a counterpoint to the above motivations, Daian asserts that

ASICs are inevitable for algorithms which are employed on sufficiently

valuable networks. Therefore they should be accepted as emergent

phenomena arising from the success of networks adopting those particular

hashing algorithms. As ASICs realise large efficiency gains over

general-purpose hardware in terms of operational costs (energy

efficiency as measured in hashes per Watt) and capital outlay (hashes

per dollar cost of ASIC) therefore lending themselves to industrial

mining facilities and the economies of scale they can access. Therefore

the reaction of forking to change hashing algorithm only provides a

temporary respite from the development of specialised hardware, and

indeed regularly scheduled tweaks may become less effective as more

versatile hardware is designed. Indeed such protocol changes may favour

well-resourced hardware manufacturers as they will be more able to

deploy capital and resources to produce new hardware. The decision

making process involved in enacting such protocol changes may also be

subject to corruption or sub-optimal outcome, as with Ethereum's chain

split following the failure of The DAO as discussed in Section 1.3

[33].

Two recent networks which took different approaches to the manifestation

of ASICs were Monero and Siacoin. Monero (XMR) is a privacy-focused

cryptocurrency with a healthy community, active developer ecosystem and

strong philosophy of maintaining decentralisation at the mining level

through the promotion of ASIC-resistance in favour of GPU mining. As XMR

nethash began to climb steeply in January and February 2018, ASIC mining

was suspected to be taking place surreptitiously, followed by

announcements by manufacturers Bitmain and Baikal that ASICs for XMR

were available for imminent shipping [34]. In April 2018, Monero

underwent its twice-annual scheduled hard fork which facilitates regular

protocol upgrade and included an adjustment to the CryptoNight hashing

algorithm to render the ASICs ineffective. Around the time of the hard

fork, XMR experienced a sudden 80 % decline in nethash with

stabilisation at around 40--50 % decline. Prior to the fork, over 90 %

of hashrate was of unknown/anonymous origin, whereas post-fork the

proportion of hashrate with unknown provenance had stabilised around

30--40 %. Therefore the level of transparency as to distribution and

provenance of computational resource increased as much as coarse

heuristics as pool activity allow inference. Some questions remain over

the methods employed to achieve consensus on the algorithm change, with

some appeals for patience or to maintain the status quo. There was also

a rather surreal incidence of extreme price volatility of the mining

equipment with fire sales as Monero's hard fork was implemented. Baikal

was advertising a "buy one, get four free" offer on the ASICs which

would have exacerbated dumping of commodity nethash on ASIC-friendly

CryptoNight networks. A number of putative breakaway Monero factions

announcing support for the original chain also announced themselves but

do appear to have largely waned into irrelevance [35].

Siacoin (SC) is a network providing secure and censorship-resistant data

storage via a decentralised P2P architecture. A hardware manufacturer

named Obelisk with strong ties to the Siacoin founders had a Blake 2b

ASIC under development and had taken a significant amount of pre-orders

for the SC1. Bitmain appears to have intercepted information relating to

this device and leveraged their economies of scale and expedience to

front-run the Obelisk miners by delivering the Antminer A3 before them

and furthermore offering aggressive discounts to Obelisk pre-order

customers. This may have been through the utilisation of faster but

sub-optimal integrated circuit development processes such as

place-and-route rather than fully-custom routing as Obelisk employed.

Unbeknownst to outsiders, Obelisk had engineering a second fallback

algorithm into their equipment so that a soft fork adjustment to the

Siacoin protocol would be sufficient to render the Bitmain ASICs

ineffective. However this was not exercised and instead an uncontentious

hard fork was conducted to recalibrate the difficult adjustment

algorithm and block time in anticipation of large increase in network

hashrate [36].

2. Research Aims and Methodology

2.1 What does Forkonomy Aim To Achieve?

As a putative analytical discipline in the early stages of development,

forkonomy is as much a perspective as a coherent set of tools and

methods at present. The notion of performing comparative analysis on

ledger forks is not new, however this somewhat high-level combination of

quantitative observation and qualitative inference is not commonly

applied to characterise the emergent phenomena exhibited in

cryptocurrencies. By taking a wider view than the present and recent

past, forkonomy aims to provide insight into the possible fates of

blockchain-oriented P2P monetary networks. A future aim is to build

sufficiently sophisticated models such that even-handed forecasts of the

probabilities of future scenarios may be elucidated from network

observation and simulation. Many of the concepts employed are borrowed

from the disciplines of astronomy, cosmology and physics, which the

author previously researched.

2.2 Research Methods and Resources

This work has relied on numerous primary and secondary data sources as

cited in the text. Blockchain analytics of BTC, BCH, ETH, ETC, XMR,

MONA, ZCL and BTCP was achieved through the use of block

explorers Blockchair.com, Blockchain.info, Etherscan.io, Etherhub.io, Bchain.info, Monerohash.com and Bitinfocharts.com with

data exported in CSV or JSON formats. This was imported into the

statistical computing suite RStudio (built upon R) for cleaning,

treatment, analysis and visualisations. Network-wide observation and

inference was conducted using publically available

sources Coin.dance for node count and

implementation versions for BTC and

BCH, Crypto51.app for ZCL and BTCP

network

hashrates, Doublespend.cash for

malleated transactions on

BCH, Coinmetrics.io for high-level

network heuristics and Onchainfx.com for

networks' token price, supply issuance and monetary policy.

3. Case Study: Advent of the Fork-Merge

3.1 Introduction

In a 2017 presentation at Breaking Bitcoin conference, Eric Lombrozo

postulated the theoretical possibility of a managed process of

convergence of chains sharing the same provenance and similar codebase

which may be thought of as a chainmerger. The idea was developed further

by Eric Wall ostensibly as potential a mechanism for BTC and BCH to

reunite post-chain split, but no prominent examples exist in the wild.

This may be subject to entropic bias, that is to say divergent paths are

those of least resistance in accordance with thermodynamics as discussed

in Section 1.3 [37].

3.2 Fork-Merge through UTXO Cross-Chain Consolidation

Building on the chainmerger concept outlined above, the notion of

a fork-merge was introduced earlier this year as the mechanism by

which a ledger fork of BTC entitled Bitcoin Private (BTCP) could be

artificially synthesised from an Equihash PoW network named Zclassic

(ZCL), itself a codebase fork of Zcash (ZEC) which in turn was

originally derived from the BTC codebase [38]. It is somewhat similar

to the "Fork + Merge" operation in Git-based repository protocols. Since

the BTC and ZCL networks possess different histories as evinced by their

unique UTXO sets and the codebase had additionally diverged further,

this was not a trivial process [39] and may be further hindered by

entropic bias. The UTXO model of ledger accounting introduced by Bitcoin

is managed by tracking the outputs of transactions as either spent or

unspent. Unspent transaction outputs contribute to coin-holders'

balances whereas spent outputs do not. In order to maintain such a

ledger, each transaction may be comprised of one or more inputs (UTXOs

with non-zero balances) and two or more outputs. This is because UTXOs

may not be partially spent, and thus any value remaining in an UTXO

after transaction is completed must be returned as a new "change" UTXO

in an analogous manner to spending a paper fiat currency banknote and

being returned different notes and coins.

The quantitative parameters underlying this cross-chain UTXO

consolidation warrant further examination. Both BTC and ZCL networks

possess equivalent relationships controlling mining subsidy emission

over time.

ZCL has a target block time of 150 seconds, block reward of 12.5 ZCL,

840000 block reward halving period (not yet reached) and 21 million ZCL

maximum supply.

BTC has a 600 second target block time with initial reward of 50 BTC per

block, though this has experienced two subsidy halvings to the present

value of 12.5 BTC per block --- with a current approximate BTC block

height of 540000 and halving period of 210000 blocks. Figure 1 displays

the characteristics of BTC mining subsidy and monetary issuance over

time.

As the time-per-halving is broadly equal on both networks the number of

halvings may be used as an approximate heuristic for the maturity of the

network. ZCL having experienced no halving to date can be considered a

young network, characterised by a high mining subsidy which incentivises

miners to secure the chain at the expense of a high effective annual

supply inflation rate of approximately 100 %, with approximately 4.5 of

21 million total ZCL coins issued. BTC is halfway between its second and

third halvings and as such can be thought of as a mature network. The

subsidy has already declined 75 % since network launch with

approximately 17 of 21 million total BTC mined and an effective annual

supply inflation of around 4 %. During periods of elevated demand for

block space, a transaction fee market has emerged which at peak times

has provided miners with greater income than the block reward [40].

This occurrence is crucial to the long-term viability of all

blockchain-based monetary networks that employ PoW for security and have

a fixed asymptotic supply curve, as the network must continue to

incentivise miners to deliver hashpower [41]. Most UTXO-based

cryptocurrencies have also adopted BTC's monetary issuance policy to

claim analogous value propositions centred around supply limitations.

By merging these UTXO sets, BTCP has synthetically created an Equihash

blockchain network with approximately 500000 of 21 million coins yet to

be issued, negligible annualised supply inflation and therefore a meagre

mining subsidy of 1.5625 BTCP, corresponding to approximately 0.0035 BTC

at time of writing. Unlike BTC however, BTCP has not been able to

bootstrap a transaction fee market, and in order to properly incentivise

miners to protect the network the transaction fees would have to be

greater than the transaction value itself.

Additional idiosyncratic risks to BTCP mining profitability arise from

possible supply shocks from involuntary coin holders who would be more

likely to commence liquidation in the event of sudden BTCP coin price

rises, and the ongoing emergence of specialised Equihash ASIC mining

hardware from multiple hardware suppliers deploying more plentiful

commodity hashrate [42].

{#nsba9btw2re}

{#nsba9btw2re}

Fig. 1. The relationship between BTC block height, mining subsidy and

supply issuance.

3.3 Forkonomics: The Impact of Fork-Merging on Monetary Networks

The fork-merge process has effectively created an elderly BTCP

blockchain between third and fourth halvings (as seen in Figure 2), with

little incentive for miners to protect and therefore minimal value

proposition as a PoW monetary network. Much of the BTCP UTXOs

involuntarily assigned to BTC UTXO owners have gone uncollected,

undoubtedly due to the low value of the 1:1 airdrop for the BTC side or

prevention of private key compromise risk. In many respects BTCP is now

experiencing an eternal post-fork hangover caused by the lopsided

incentive structures engineered into the fork-merge. The event

asymmetrically benefited ZCL holders which had a much lower per coin

price than BTC but also entitled holders to a 1:1 airdrop. This was

particularly the case for those who held ZCL balances prior to the

announcement of the fork-merge, as the market price of ZCL experienced

an approximate hundredfold increase in USD terms within a 30 day period

prior to the fork-merge [43].

Due to the disparity in mining subsidy value and network age (not

"effective maturity" as discussed above) between ZCL and BTCP, ZCL

appears to retain a reasonably cohesive constituency of stakeholders ---

miners, exchanges, users and so on --- despite many developers

abandoning the project at time of fork. In contrast, BTCP seems to have

lost most of its pre-fork proponents and has failed to acquire listing

on major exchanges to access liquidity in order to improve its value

proposition as a speculative asset. BTCP vs ZCL may be considered an

extreme case of fork-induced emission curve fatigue. That is to say

that the fork-merge process has resulted in a cryptocurrency network

simultaneously vulnerable to majority attacks and unable to bootstrap

itself into a secure and reliable state as the block subsidy available

in an elderly network does not sufficiently incentivise computational

resource in the absence of an on-chain transaction fee market. The lack

of evidence of such attacks on BTCP may be due to the lack of on-chain

transaction volume and associated fiat equivalent value making even a

low-cost attack a waste of resource. Furthermore trading platforms do

appear to anticipate the likelihood of such an attack as typically

25--50 confirmations are required to consider a BTCP deposit confirmed

and spendable at an exchange.

In 2018 there has been an emerging trend of ledger forks of BTC

possessing greatly inflated market capitalisations in comparison to

codebase forks with virgin genesis blocks and ledgers. This is at least

in part due to the effective sequestration of large proportions of the

supply, essentially attention-locked since BTC UTXO owners have neither

financial nor ideological motivation to participate at the potential

expense and inconvenience of accessing private keys. Observable on-chain

transaction volume (not including shielded transactions which typically

constitute a tiny minority of usage) is minimal on both BTCP and ZCL

networks with significantly under one million USD average daily volume,

whilst BTC moves approximately several billion USD equivalent per day.

In terms of hashrate ZCL has approximately 25 times more network

hashrate than BTCP with a nominal market capitalisation of 3 times less

[44]. The consequence of this is that the BTCP chain is rendered

extremely vulnerable to 51 % attacks with a trivial vector employing

rented hashrate --- using figures at time of writing the 1 hour cost of

a majority attack was approximately 200 USD. For a network with a

nominal value (using market capitalisation as a coarse heuristic) of

approximately one hundred million USD, the prospect for transaction

disruption seems sufficiently high to preclude any realistic proposition

of BTCP as a monetary network. If majority takeovers become trivial in a

cryptocurrency network, exchanges will be reticent to list it as they

would be the primary victims of double-spending attacks when not

requiring sufficient confirmations for transaction finality to be beyond

doubt [45].

{#nan4sqynkiu}

{#nan4sqynkiu}

Fig. 2. Generalised emission curve and supply schema for cryptocurrency

networks deriving their accounting and monetary characteristics from

Bitcoin. Each "step down" represents a halving of block subsidy, halving

in effective supply inflation rate and an advancement in the lifecycle

phase of a blockchain network. Emission curve and supply schema for ZCL

(blue), BTC (green) and BTCP (orange) networks compared visually.

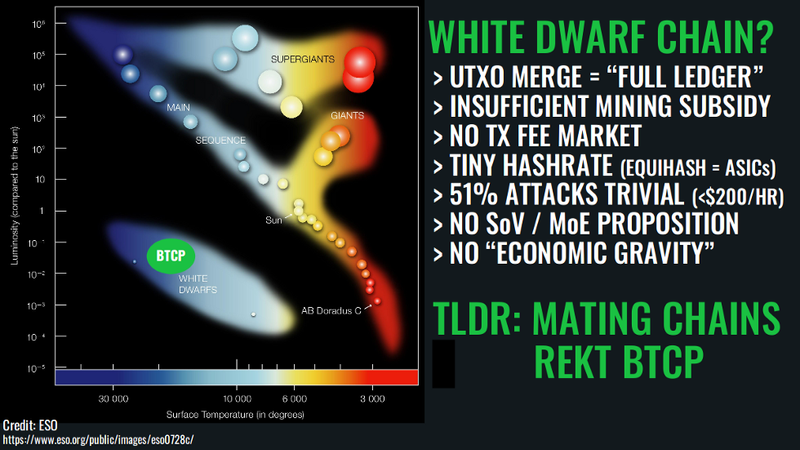

4. Discussion: Implications for Ageing Blockchains and Prominent Minority Forks

The emission curve fatigue that BTCP is experiencing, combined with lack

of transaction fee market results in an insecure network with absent

value proposition. Indeed this is one of the possible futures for any

elderly PoW blockchain. By analogy with stellar lifecycles, the

moniker white dwarf chain may be applied to BTCP. In common with the

celestial remnant, high maturity and low economic gravity prevent the

network from attracting substantive accretion, eventually no longer

possessing the critical mass to function. There is a prospect that BTCP

will attempt a transition to PoS or dPoW in order to seek refuge from

thermodynamic attacks. Recently the prospect of confiscation of

"inactive" UTXOs in order to liberate coin supply from attention-locked

holders of BTCP in order to provide further miner subsidy in order to

attract greater hashrate has emerged [39]. The disingenuous trope of

"Satoshi's Vision" was invoked by BTCP proponents in the pre-fork

marketing, though it is difficult to see how Satoshi Nakamoto's

cypherpunk principles were respected and honoured through the mechanism

of confiscating UTXOs under his control.

An alternative outcome termed a chain death spiral is also a possibility

for BTCP. Should Equihash resource be sufficiently incentivised to be

directed elsewhere, the network may stop issuing blocks altogether. This

was a particular concern for BTC at the time of the BCH chain split,

though ironically it was BCH that produced severely tardy blocks with

block intervals reaching many hours for some time. This was due to the

BCH network inheriting the BTC network's difficulty whilst only

possessing a fraction of the former BTC hashrate. A customised

difficulty adjustment algorithm was invoked to rapidly adjust the BCH

network difficulty downwards to reflect the much lower nethash of the

minority SHA-256 BCH network fragment. The lack of such a difficulty

adjustment mechanism in BTC beyond the original specification's 2016

block window came to be perceived as a potential attack vector from a

hostile ledger fork [46].

The significance of implications arising from the BTCP case study are

due to the lack of organically elderly blockchain networks in existence

today. Emergent behaviours that are observed in these distributed

environments may vary from hypothetical studies utilising

cryptoeconomic, distributed systems or game theoretical perspectives.

Due in part to the BCH difficulty adjustment process --- and successor

algorithms performing analogous functions --- BTC and BCH have already

diverged by approximately seven thousand blocks chain length (Figure 3)

which corresponds to around 50 days greater effective age of BCH in the

year since chain split. The consequence is that, ceteris paribus, the

BCH blockchain will reach its next block subsidy halving sooner than

BTC. Coupled with the fact that BCH shares the SHA-256 mining algorithm

with BTC but now has approximately ten times less hashrate (Figure 4),

there is declining economic incentive for miners to secure the minority

BCH network [47]. With no fix currently implemented for transaction

malleability due to BCH's rejection of SegWit and no alternative ready

to deploy, 51 % attacks have become trivial to conduct by several BTC

mining pools and double spent transactions are growing in frequency,

calling any notion of monetary soundness or payment utility proposition

into serious question [48].

{#nvbxcanryrm}

{#nvbxcanryrm}

Fig. 3. Chain dynamics of BTC (blue) and BCH (red) networks August

2017--18, as visualised through the benchmarking of "chain time" versus

Earth time. Data from Blockchair.com.

{#n8y12g0skox}

{#n8y12g0skox}

Forkonomy assessment of BTCP (Aug/Sep 2018)

Through the observation of networks which in the past competed for ASIC

hashrate such as Litecoin and Dogecoin, it has been observed that once

the security of a PoW network sharing a mining algorithm with a dominant

competitor is believed to be compromised, two main categories of

remedial action may be utilised. To preserve decentralisation and

network sovereignty, the adoption of an alternative and unique PoW

algorithm is an option but would be unpalatable for an ASIC-oriented

network such as BCH. An alternative is to implement merge-mining whereby

PoW on the dominant network for a particular algorithm counts towards

PoW on the merge-mined network [49], or periodic checkpoint

notarisation - also known as delayed PoW - of latest block hash into the

most secure blockchain as utilised by minority Equihash network Komodo

[50]. Confiscation of "inactive" UTXOs or account balances has also

been proposed by minority forks such as United Bitcoin and Bitcoin

Private as discussed above.

The canonical Ethereum network ETC may have a different future to the

typical minority branch, as development paths between forks have

diverged and ETH intends to attempt transition to PoS with the Casper

family of consensus protocols [51], accompanied by a significant

reduction in block issuance subsidy to 0.6 ETH per block [52]. Should

this occur as multiple competing Ethash ASICs and high performance FPGA

bitstreams are distributed more widely, ETC may retain a strong value

proposition as the canonical, decentralised and immutable Ethereum

network with a sound monetary policy and thermodynamically assured

network security. As Figure 5 shows, ETH has an annual equivalent supply

inflation of approximately 7.5 % and no maximum limit on token supply,

whereas ETC's inflation is around 5.75% and projected to decrease much

more rapidly due to a fixed supply limit. ETC has also removed the

so-called difficulty bomb which is intended to disincentivise mining by

making it increasingly unprofitable.

{#nccybz08kgf}

{#nccybz08kgf}

Fig. 4. Difficulty (as proxy heuristic for hashrate) comparision of BTC

(black) and BCH (grey) networks August 2017--18. Data from

Blockchair.com

{#nozntshd94m}

{#nozntshd94m}

Fig. 5. All-time supply inflation comparison of ETC (black) and ETH

(grey). Data from ECIP1017 [53].

5. Future Perspectives on Forks

As with any novel field of study many open questions remain as to how

new technologies, emergent phenomena and threats caused by internal

factions within open source protocol networks or external entities such

as rival blockchains, lawmakers and silicon foundries may influence the

forking tendencies of cryptocurrency networks. Sztorc's notion of fork

futures has merit insofar as competing visions may be assessed and

priced in real time by the marketplace prior to implementation. This

facilitates the assessment of support for the various options proposed

by competing factions, potentially preventing quite a substantial

proportion of chain splits by using the market to assess the value of

competing ideas. [54].

Velvet forks as proposed by Kiayias et al. could help mitigate potential

network consensus failures by increasing inclusiveness and compatibility

of protocol upgrades, by being minimally invasive with respect to

network participants not running the velvet fork upgrade [28]. An

example of successful implementation of a velvet fork has been found in

decentralised mining pool P2Pool's sharechain, which keeps track of

mining shares which correspond to block hashes close to but not below

the network difficulty limit. In order to reduce reward variance for

individual participants in the mining pool, shares are kept track of by

the sharechain [55].

The ongoing litigation against the cryptocurrency exchange Bitgrail

involves an attempt to legally enforce a rollback of the Nano (formerly

Raiblocks) block-lattice network to reclaim tokens which were lost due

to software vulnerabilities. It is hard to envisage an outcome whereby a

legal pronouncement is made which carries sufficiently global or

borderless jurisdiction to coerce large constituencies of a network to

behave contra to their incentives. Most likely this would trigger a

factional network disintegration event [56].

Hypothesising more broadly, as the canon of forkonomy expands to include

new and emergent phenomena there may develop further aesthetic

disciplines with which to codify, classify and characterise

trust-minimised network partitions in all their forms. As with celestial

outcomes, the interplay of enthalpy and entropy could provide a

generalised basis for modelling the fate of cryptocurrency networks and

further work is underway in this area. Moving from the ontological and

observational basis presented here as forkonomy (by analogy with

astronomy) and forkonomics (by analogy with economics), epistemological

treatises may be considered forkology [57] and philosophical

approaches forkosophy.

Acknowledgements

Thanks to numerous esteemed colleagues for proof-reading, comments and

corrections.

References

-

List of Linux Distributions,

Wikipedia. https://en.wikipedia.org/wiki/List_of_Linux_distributions.

Last accessed 10 August 2018. -

Nakamoto, S. (2008) Bitcoin: A Peer-to-Peer Electronic Cash

System. http://bitcoin.org/bitcoin.pdf. -

Delgado-Segura, S., Prez-Sol, C., Navarro-Arribas, G., and

Herrera-Joancomart, J. (2017) Analysis of the Bitcoin UTXO set. IACR

Cryptology ePrint Archive, 1095. https://eprint.iacr.org/2017/1095.pdf -

BCH Node Status, Coin

Dance. https://cash.coin.dance/nodes#nodeVersions. Last accessed 10

August 2018. -

Metcalfe, B. (2013) Metcalfe's Law after 40 Years of Ethernet. In:

Computer, vol. 46, no. 12,

26--31. https://doi.org/:10.1109/MC.2013.374. -

Bonneau, J. (2018) Hostile Blockchain Takeovers. In Bitcoin '18:

Proceedings of the 5th Workshop on Bitcoin and Blockchain Research. -

Mark, D., Zamfir. V., and Sirer, E. G. (2016) A Call for a Temporary

Moratorium on The

DAO, http://hackingdistributed.com/2016/05/27/dao-call-for-moratorium. -

BitMEX Research (2018) Revisiting The

DAO, https://blog.bitmex.com/revisiting-the-dao. -

Buterin, V. (2017) Notes on Blockchain

Governance, https://vitalik.ca/general/2017/12/17/voting.html. -

van Wirdum, A. (2016) Ethereum Classic Community Navigates a

Distinct Path to the

Future, https://bitcoinmagazine.com/articles/ethereum-classic-community-navigates-a-distinct-path-to-the-future-1471620464/. -

Conner, E. (2018) EIP 1234: A Case For Ethereum Block Reward

Reduction in

Constantinople, https://medium.com/@eric.conner/a-case-for-ethereum-block-reward-reduction-in-constantinople-eip-1234-25732431fc77. -

Ethereum Uncle Rates,

Etherscan. https://etherscan.io/chart/uncles. Last accessed 10 August -

Eyal, I., and Sirer, E. G. (2014) Majority is Not Enough: Bitcoin

Mining is Vulnerable. In International Conference on Financial

Cryptography and Data Security, 436--454. Springer, Berlin, Heidelberg. -

Grunspan, C., and Perez-Marco, R. (2018) On Profitability of

Selfish Mining. IACR Cryptology ePrint Archive, 1805. -

Bitcoin Empty Blocks

Blockchair. https://blockchair.com/bitcoin/blocks?s=size(asc). Last

accessed 10 August 2018. -

Monacoin Block

Explorer. https://bchain.info/MONA/. Last

accessed 10 August 2018. -

Nayak K., Kumar, S., Miller, A., and Shi, E. (2016) Stubborn

Mining: Generalizing Selfish Mining and Combining with an Eclipse

Attack. IEEE European Symposium on Security and Privacym 305--320.

EuroS&P,

Saarbrucken. https://doi.org/:10.1109/EuroSP.2016.32 -

Zhang, R., and Preneel, B. (2017) Publish or Perish: A

Backward-compatible Defense against Selfish Mining in Bitcoin. In

Cryptographers' Track at the RSA Conference, 277--292. Springer, Cham. -

Miller, A. (2013) Feather-forks: enforcing a blacklist with sub-50%

hash power. https://bitcointalk.org/index.php?topic=312668.0. Last

accessed 10 August 2018. -

Hacken (2017) The Rush for

Hashpower. https://hacken.io/wp-content/uploads/The-Rush-for-Hashpower.pdf. Last

accessed 10 August 2018. -

Sclavounis, O. (2017) Understanding Public Blockchain

Governance, https://www.oii.ox.ac.uk/blog/understanding-public-blockchain-governance -

BitMEX Research (2018) Covert versus overt

AsicBoost, https://blog.bitmex.com/graphical-illustration-of-a-bitcoin-block -

Hilliard, J. (2017)

BIP91, https://github.com/bitcoin/bips/blob/master/bip-0091.mediawiki. Last

accessed 10 August 2018. -

Ver, R. (2018) Why I Think Bitcoin Cash is

Bitcoin, https://www.yours.org/content/why-i-think-bitcoin-cash-is-bitcoin-6cb2dda7ca08 -

O'Hagan, A. (2016), The Satoshi

Affair, https://www.lrb.co.uk/v38/n13/andrew-ohagan/the-satoshi-affair -

Castor, A. (2018) No

Incentive, https://www.coindesk.com/no-incentive-algorand-blockchain-sparks-debate-cryptography-event -

Poelstra, A. (2016) A Treatise on

Altcoins, https://download.wpsoftware.net/bitcoin/alts.pdf -

Kiayias, A., Miller, A., and Zindros, D. (2018) Non-interactive

Proofs of Proof-of-work. IACR Cryptology ePrint

Archive, https://eprint.iacr.org/2017/963.pdf -

Decred Politeia Github, https://github.com/decred/politeia. Last

accessed 10 August 2018. -

Crystal Blockchain

Analytics, https://crystalblockchain.com. Last

accessed 10 August 2018. -

Sayres, N. (2018) Bitmain Faces New Accusations of Secret

Mining, https://hacked.com/bitmain-faces-new-accusations-of-secret-mining/.

Last accessed 10 August 2018. -

BitMEX Research (2018) New Ethereum Miner Could be a Game

Changer, https://blog.bitmex.com/nextstageinmining. Last accessed 10

August 2018. -

Daian, P. (2018) Anti-ASIC Forks Considered

Harmful, https://pdaian.com/blog/anti-asic-forks-considered-harmful. Last

accessed 10 August 2018. -

Wilmoth, J. (2018) Manufacturer Holds CryptoNight ASIC Firesale

after Monero Hard

Forks, https://www.ccn.com/manufacturer-holds-cryptonight-asic-firesale-after-monero-hard-forks. Last

accessed 10 August 2018. -

Source:

Bitinfocharts, https://bitinfocharts.com/comparison/monero-hashrate.html. Last

accessed 10 August 2018. -

Vorick, D. (2018) The State of Cryptocurrency

Mining, https://blog.sia.tech/the-state-of-cryptocurrency-mining-538004a37f9b.

Last accessed 10 August 2018. -

Lombrozo, E. (2017) Speech at Breaking Bitcoin

Conference, https://www.youtube.com/watch?v=0WCaoGiAOHE -

Biryukov, A., and Khovratovich, D. (2016) Equihash: Asymmetric

Proof-of-Work Based on the Generalized Birthday

Problem. https://eprint.iacr.org/2015/946 -

Bitcoin Private

Whitepaper, https://btcprivate.org/whitepaper.pdf. Last accessed 10

August 2018. -

Bitcoin Block 500439, Source: Blockchair

Explorer, https://blockchair.com/bitcoin/block/500439. Last accessed

10 August 2018. -

Ammous, S. (2018) The Bitcoin Standard: The Decentralized

Alternative to Central Banking. John Wiley & Sons. -

Let's talk about ASIC mining, Zcash

Forum, https://forum.z.cash/t/let-s-talk-about-asic-mining/27353. Last

accessed 10 August 2018. -

Source: OnChainFX, https://onchainfx.com/asset/zclassic. Last

accessed 10 August 2018. -

Source: MiningSpeed Pool

Monitor, https://pool.miningspeed.com. Last

accessed 10 August 2018. -

Source: PoW 51% Attack

Cost, https://www.crypto51.app. Last

accessed 10 August 2018. -

Wong, J. I., Bitcoin cash could lead to bitcoin "death spiral",

Quartz, https://qz.com/1127817/bitcoin-cash-bch-price-could-lead-to-bitcoin-death-spiral -

Source:

Blockchair, http://www.blockchair.com. Last

accessed 10 August 2018. -

Source: BCH Doublespend

Monitor, http://doublespend.cash. Last

accessed 10 August 2018. -

Judmayer, A., Zamyatin, A., Stifter, N., Voyiatzis, A. G., and

Weippl, E. (2017) Merged Mining: Curse or Cure? In Data Privacy

Management, Cryptocurrencies and Blockchain Technology, 316--333.

Springer, Cham. -

Delayed Proof of Work

Whitepaper, https://github.com/SuperNETorg/komodo/wiki/Delayed-Proof-of-Work-(dPoW)-Whitepaper -

Casper Ethereum Github, https://github.com/ethereum/casper. Last

accessed 10 August 2018. -

Griffith, V., and Buterin, V. (2017) Casper the Friendly Finality

Gadget, https://arxiv.org/pdf/1710.09437.pdf -

Mazur, M. (2016)

ECP1017, https://github.com/ethereumproject/ECIPs/pull/20/files. Last

accessed 10 August 2018. -

Sztorc, P. (2017) Fork Futures (via the

Exchanges), http://www.truthcoin.info/blog/fork-futures/ -

Zamyatin, A., Stifter, N., Judmayer, A., Schindler, P., Weippl E.,

and Knottenbelt W. (Short Paper) A Wild Velvet Fork Appears! Inclusive

Blockchain Protocol Changes in Practice. In Bitcoin '18: Proceedings of

the 5th Workshop on Bitcoin and Blockchain Research. -

Gordon, S. (2018) Nano Team Target of Cryptocurrency Class Action

Lawsuit, https://bitcoinmagazine.com/articles/nano-team-target-cryptocurrency-class-action-lawsuit/ -

Antonopoulos, A. M. (2017) Forkology: A Study of

Forks, https://www.youtube.com/watch?v=rpeceXY1QBM.